Su carrito está vacío

Carrito

If you make between $50,000 and $150,000 a year but still feel broke...

You're not alone.

And more importantly: it's not your fault.

After 12 years as a financial therapist working exclusively with middle-class families, I've identified six invisible money traps that keep good people stuck in the paycheck-to-paycheck cycle.

These aren't the typical "stop buying lattes" lectures you've heard a thousand times.

These are systemic issues built into how we're taught to manage money in America—and they're costing you years of financial freedom.

The worst part? You probably don't even realize you're caught in them.

I'm Sarah Chen. I've been a Certified Financial Planner and Financial Therapist in Seattle for 12 years.

Last year, I analyzed the financial patterns of 847 middle-class clients who came to me feeling like failures despite "doing everything right."

Good jobs. Responsible people. Many had college degrees and professional careers.

Yet 83% had less than $1,000 in savings. 67% carried credit card debt. And 91% told me they felt shame about their finances.

When I dug deeper, I discovered that nearly all of them were caught in the same six traps.

Once I showed them how to escape these traps, everything changed.

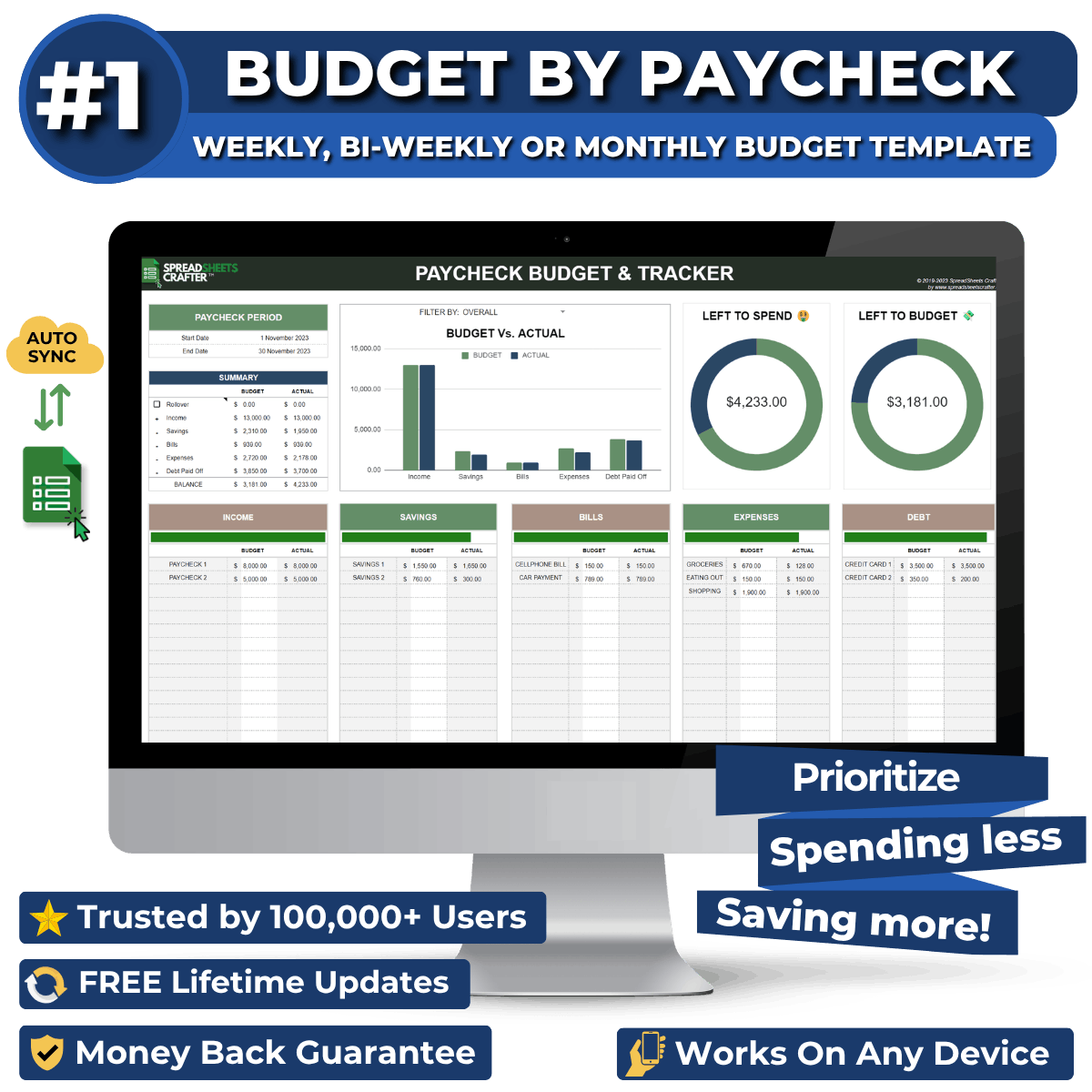

Here's what they don't tell you about monthly budgets: they don't match how you actually live.

You get paid every two weeks (or weekly, or twice a month). But your budget pretends you get paid on the 1st of every month.

Your rent is due on the 1st. Your car payment on the 7th. Your insurance on the 15th. Your credit card on the 23rd.

But your paychecks arrive on the 6th and 20th.

See the problem?

This mismatch creates what I call "phantom money"—you think you have money for groceries, but that money is actually already spoken for by bills that haven't hit yet.

Then you overspend. Then you feel guilty. Then you give up on budgeting entirely.

The result: 78% of my clients who used monthly budgets abandoned them within 90 days.

You're 18 days into the month. You've already blown your budget. You tell yourself, "I'll start fresh on the 1st."

But here's what happens: the 1st arrives, you're motivated for three days, something unexpected happens on the 4th, and by the 8th you're already thinking about starting over "next month."

I've watched clients spend YEARS in this cycle.

The problem isn't your discipline. The problem is that monthly cycles are too long for behavior change. You need more frequent "fresh starts" to build sustainable habits.

The result: My clients averaged 4.3 "I'll start over next month" resets per year before they became completely demoralized.

You're not spending $200/month on subscriptions because you're irresponsible.

You're spending it because every company in America has shifted to subscription models designed to be invisible.

Netflix. Spotify. Amazon Prime. iCloud storage. Gym membership. Meal kit. Streaming services you forgot about. Apps that auto-renewed. That software you used once.

The average middle-class household now spends $273/month on subscriptions. That's $3,276 per year.

But here's the real trap: they hit different credit cards on different days, so you never see the total impact.

It's not one big painful purchase. It's death by a thousand paper cuts.

The result: When I audit subscriptions with clients, we find an average of $847 in annual subscriptions they either forgot about or "meant to cancel."

Car insurance every 6 months. Amazon Prime annually. Holiday gifts in December. Back-to-school expenses in August. Birthday parties. Car registration. Vet bills.

These aren't emergencies. They're predictable irregular expenses.

But traditional monthly budgets treat them like surprises. So when they hit, you think "this is an emergency" and put them on a credit card.

Over time, these "surprises" become the primary driver of credit card debt.

I had a client with $14,000 in credit card debt. We traced it back. Not one purchase was frivolous. It was 100% predictable expenses that she hadn't planned for within her monthly budget.

The result: 73% of middle-class credit card debt comes from irregular expenses that could have been predicted and planned for.

You make good money. But you're always stressed about money.

Why? Because you don't have a cash flow problem—you have a cash flow timing problem.

This is the trap that destroys people who make six figures but still live paycheck to paycheck.

Your annual income is fine. But three of your biggest bills hit in the first paycheck period, so you're broke for two weeks. Then you overcompensate in the second period and there's nothing left for irregular expenses.

Traditional budgets show you monthly totals. They don't show you which paycheck is drowning while the other one is floating.

The result: 64% of my clients making over $100,000 had unbalanced paycheck allocations that created artificial scarcity.

You've downloaded Mint. Or YNAB. Or EveryDollar. Or three others.

You set up all the categories. Synced your accounts. Felt optimistic for 48 hours.

Then you stopped opening the app because every notification made you feel like a failure.

Here's what the personal finance industry doesn't want you to know: their apps are designed for compliance, not psychology.

They gamify guilt. They send notifications that trigger shame. They show you colorful charts of your failures.

Most budget apps increase financial anxiety rather than reduce it.

I've had clients cry in my office because they had 400+ unread notifications from Mint. Each one a small reminder that they're "bad with money."

The result: 94% of people who download budgeting apps abandon them within 90 days. The apps work great—for the 6% who already have good money habits.

When I analyzed my client data, the pattern was devastating:

Clients caught in 4+ of these traps:

But here's the important part: none of this was their fault.

These are structural problems with how we're taught to budget. It's not about discipline or intelligence.

It's about using a system that actually works with your life instead of against it.

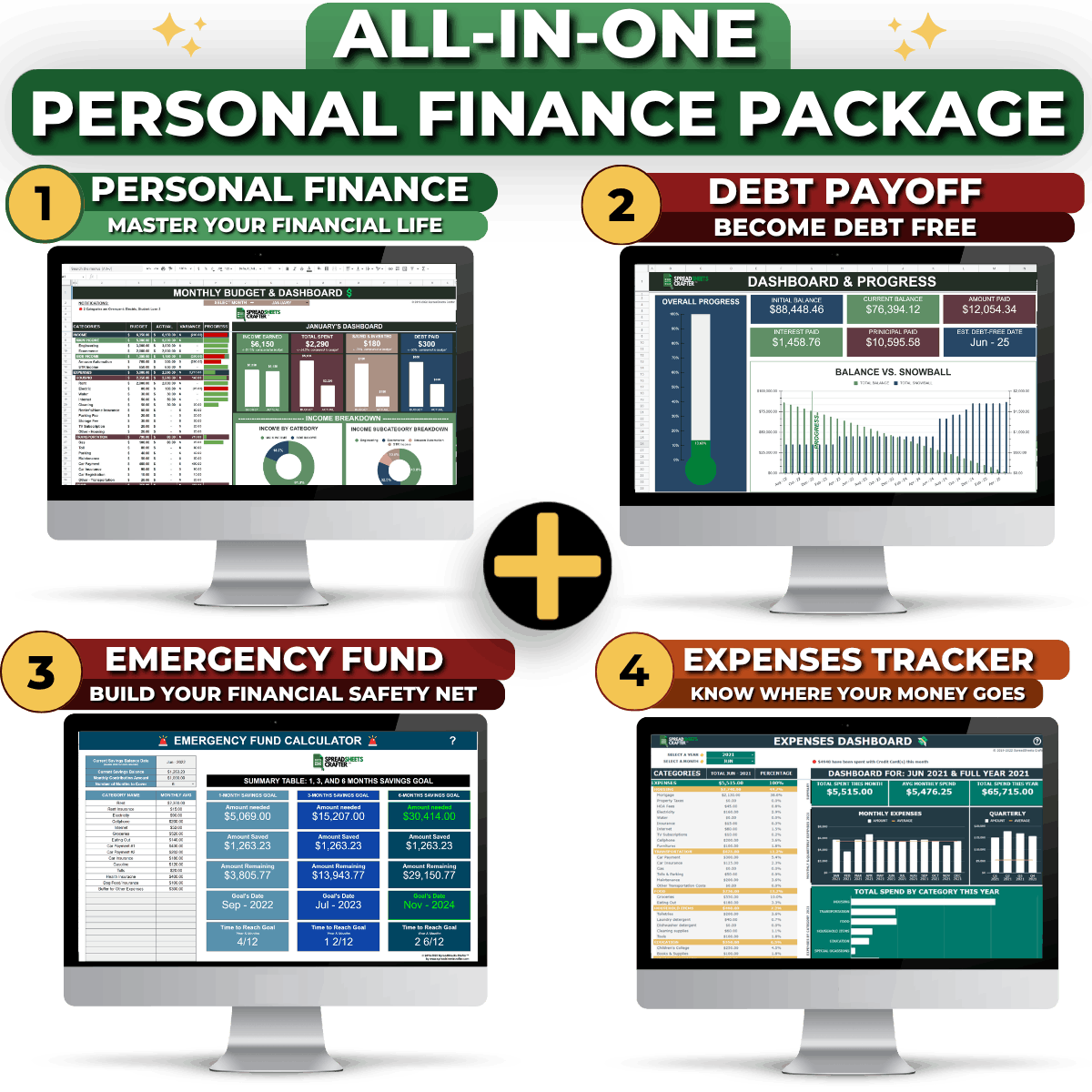

After discovering these six traps, I spent eight months developing a framework that addressed every single one.

Not a monthly budget. Not another app full of categories. Not another "try harder" system.

A paycheck-based money management system that eliminates all six traps simultaneously.

Here's how it works:

The Paycheck-Based Framework

I tested this framework with 35 clients who were stuck in multiple traps. People who'd tried everything and felt hopeless.

The results shocked me.

After 90 Days:

One client texted me: "For the first time in my life, I know exactly where my money is going. It's like someone turned the lights on."

Another said: "I've been making $95,000 for three years and always felt broke. Turns out, 70% of my bills were hitting one paycheck. Once I rebalanced, I suddenly had breathing room."

Here's the problem: I developed this framework in my therapy practice, but I couldn't scale it. The math was too complex. The personalization was too intensive.

I needed software that could handle paycheck-based budgeting with all six trap solutions built in.

I searched for months. Tested dozens of tools.

Then I found the Budget by Paycheck.

It was the only system that incorporated every element of the framework I'd developed. Not similar. Not inspired by. The exact methodology I use with private clients who pay thousands for financial therapy.

I now recommend it to every single client.

If you want to escape these six traps without another complicated system you'll abandon in 60 days... you need to act now.

Budget by Paycheck is gaining attention fast. A major personal finance publication is planning a feature next month that will reach 2 million+ readers.

Right now, you can still get Budget by Paycheck at the introductory price—but availability may be limited after the feature publishes.

ESCAPE THE 6 TRAPS NOW →The Cost of Staying Trapped:

For less than the cost of one month's subscription creep (average: $273), you can escape all six traps permanently.

The choice is yours: stay caught in traps designed by an industry that profits from your struggle, or finally break free.

GET THE BUDGET BY PAYCHECK NOW →I wish someone had shown my clients these traps before they spent years feeling like failures.

Don't waste another year stuck in systems that weren't designed for you. Your financial freedom—and your peace of mind—depends on the choice you make right now.

Don't let another year pass while you're caught in traps that aren't your fault.